Are you wondering how much money you should save each month? It’s a common question that many people have, and finding the right answer can be a bit tricky. But fear not! In this article, we’ll dive into the world of personal finance and explore some tips and guidelines to help you determine the optimal amount to save each month. So, grab your favorite beverage, sit back, and let’s get started on this savings journey together!

When it comes to saving money, there isn’t a one-size-fits-all answer. The amount you should save each month depends on a variety of factors, such as your income, expenses, financial goals, and lifestyle. It’s important to strike a balance that allows you to save for the future while still enjoying the present. After all, life is about finding that sweet spot between planning for tomorrow and living for today.

So, whether you’re just starting your savings journey or looking to revamp your current strategy, we’ve got you covered. In the following paragraphs, we’ll explore some practical tips and insights to help you determine how much money you should save each month. Get ready to take control of your finances and pave the way for a brighter future!

When it comes to saving money each month, there is no one-size-fits-all answer. The amount you should save depends on your individual financial goals and circumstances. However, financial experts generally recommend saving at least 20% of your monthly income. This ensures you have enough for emergencies, future expenses, and retirement. If you’re struggling to save that much, start with a smaller percentage and gradually increase it over time. Remember, every little bit adds up, so even saving a small amount is better than saving nothing at all.

How Much Money Should You Save Each Month?

When it comes to personal finance, one of the most important habits to develop is saving money. But how much should you actually be saving each month? The answer to this question can vary depending on your individual financial situation and goals. In this article, we will explore some factors to consider when determining how much money you should save each month.

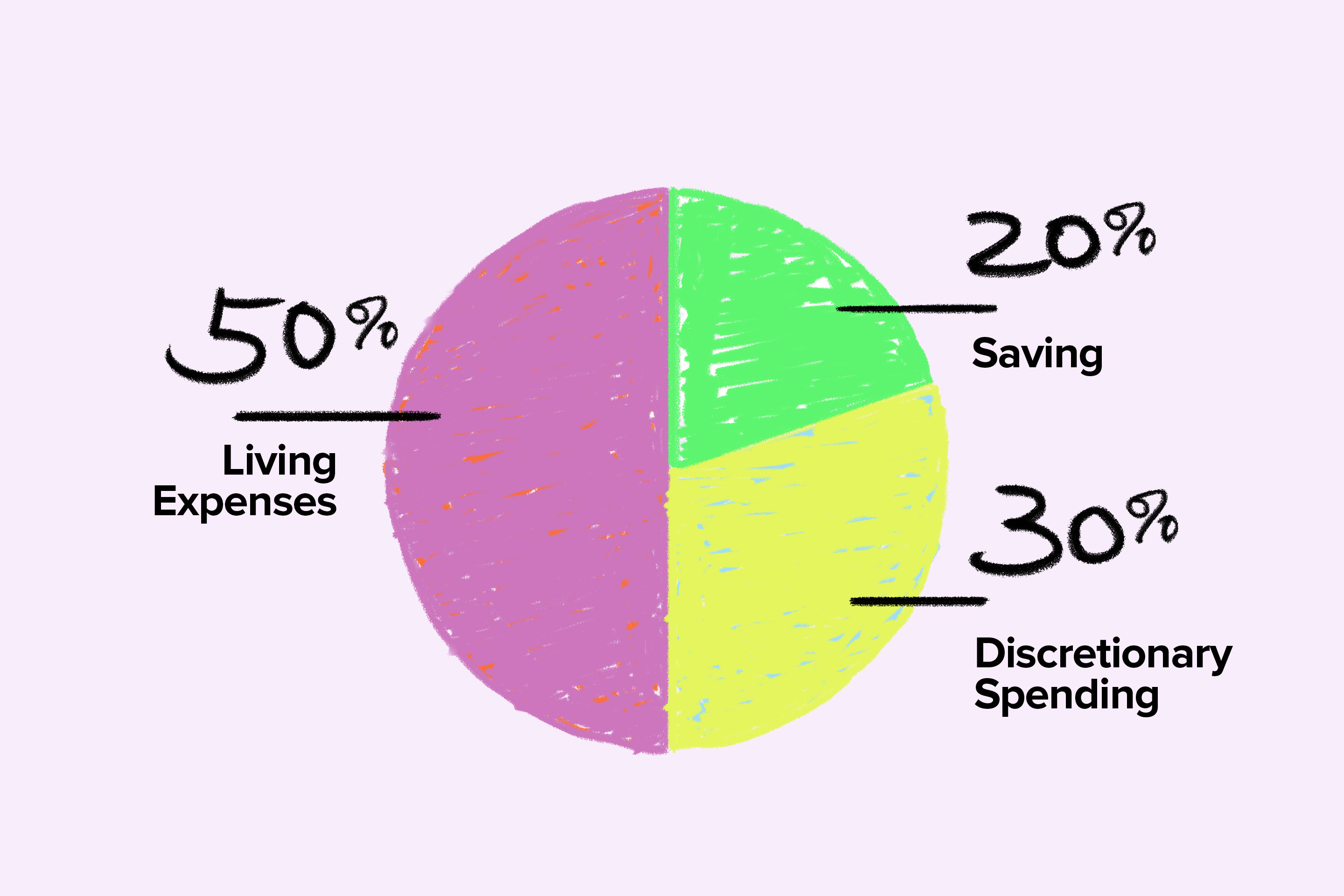

The 50/30/20 Rule: A Popular Budgeting Approach

One popular budgeting approach is the 50/30/20 rule. This rule suggests that you allocate 50% of your income to essential expenses, 30% to discretionary spending, and 20% to savings. This can provide a helpful guideline for determining how much you should save each month. By following this rule, you ensure that you are saving a significant portion of your income while still allowing yourself some flexibility for non-essential expenses.

However, it’s important to note that the 50/30/20 rule may not work for everyone. Depending on your financial goals and obligations, you may need to adjust the percentages to better suit your needs. It’s essential to evaluate your personal situation and make adjustments accordingly.

Factors to Consider

While the 50/30/20 rule is a good starting point, there are several factors you should consider when determining how much money you should save each month. These factors include:

1. Your Income

Your income plays a significant role in how much you can save each month. If you have a higher income, you may be able to save a larger percentage of your earnings. On the other hand, if you have a lower income, you may need to prioritize your expenses and save a smaller percentage.

It’s important to strike a balance between saving and covering necessary expenses. If you find it challenging to save a substantial amount, consider ways to increase your income or reduce your expenses.

2. Financial Goals

Your financial goals also impact how much you should save each month. If you have specific goals, such as buying a house or saving for retirement, you may need to save a higher percentage of your income. It’s essential to determine your goals and create a savings plan that aligns with them.

By setting clear objectives, you can prioritize your savings and work towards achieving your long-term financial aspirations.

3. Expenses and Debts

Your monthly expenses and debts also play a role in determining how much money you should save. If you have significant expenses or debts to pay off, you may need to adjust your savings accordingly. It’s crucial to balance your financial obligations while still setting aside money for savings.

Consider creating a budget to track your expenses and identify areas where you can cut back. By reducing unnecessary expenses, you can free up more money to put towards savings.

4. Emergency Fund

Building an emergency fund is an essential aspect of financial planning. An emergency fund provides a safety net in case of unexpected expenses or financial hardships. It’s recommended to save three to six months’ worth of living expenses in your emergency fund.

When determining how much money you should save each month, make sure to prioritize building your emergency fund. Set aside a portion of your income specifically for this fund until you reach your desired savings goal.

Establishing a Realistic Savings Goal

While there is no one-size-fits-all answer to how much money you should save each month, it’s crucial to establish a realistic savings goal based on your individual circumstances. By considering factors such as your income, financial goals, expenses, and emergency fund, you can create a savings plan that works for you.

Remember that saving money is a long-term commitment, and it’s important to be consistent with your savings efforts. Start by setting a realistic savings goal and gradually increase it over time as your financial situation improves.

Conclusion

Determining how much money you should save each month is a personal decision that depends on various factors. The 50/30/20 rule can provide a helpful guideline, but it’s essential to consider your income, financial goals, expenses, and emergency fund when setting a savings goal. By creating a realistic and achievable plan, you can develop a healthy savings habit and work towards your long-term financial success.

Key Takeaways

- 1. Start saving early to take advantage of compound interest.

- 2. Aim to save at least 20% of your monthly income.

- 3. Create a budget to track your expenses and identify areas to cut back.

- 4. Set specific savings goals to stay motivated.

- 5. Automate your savings by setting up automatic transfers to a separate savings account.

Frequently Asked Questions

Here are some common questions people have about how much money to save each month:

1. What factors should I consider when determining how much money to save each month?

When deciding how much money to save each month, it’s important to consider your income, expenses, financial goals, and any debt you may have. Start by calculating your monthly income and subtracting your necessary expenses, such as rent or mortgage, utilities, and groceries. Assess your financial goals, whether it’s saving for retirement, buying a house, or an emergency fund. Take into account any outstanding debts, such as student loans or credit card balances, and allocate a portion of your monthly savings towards debt repayment.

Additionally, it’s crucial to have a budget in place to track your spending and identify areas where you can cut back to save more. Regularly reviewing and adjusting your savings plan is essential as your financial situation and goals may evolve over time.

2. Is there a general rule of thumb for how much money I should save each month?

While there isn’t a one-size-fits-all answer, financial experts often recommend saving at least 20% of your income each month. This includes contributions towards retirement savings, emergency fund, and other financial goals. However, this percentage may vary depending on individual circumstances, such as your age, income level, and financial obligations.

If saving 20% seems unattainable, start with a smaller percentage and gradually increase it over time. The important thing is to develop a consistent saving habit and make it a priority in your financial planning.

3. How can I determine a realistic savings goal?

Setting a realistic savings goal involves assessing your financial priorities and considering your long-term plans. Start by identifying your short-term and long-term financial goals, such as buying a home, starting a business, or retiring comfortably. Research the costs associated with these goals and break them down into manageable savings targets.

Consider your timeline for achieving these goals and calculate how much you need to save each month to reach them. Be sure to account for inflation and any potential changes in your income or expenses. It’s important to strike a balance between saving for the future and enjoying your present financial needs.

4. How can I save more money each month?

There are several strategies you can implement to save more money each month. Firstly, create a budget to track your spending and identify areas where you can cut back. Look for opportunities to reduce discretionary expenses, such as eating out, entertainment, or unnecessary subscriptions.

Automate your savings by setting up automatic transfers from your checking account to a separate savings account. This ensures that a portion of your income goes directly towards savings without temptation to spend it. Additionally, consider finding ways to increase your income, such as taking on a side gig or negotiating a raise at work. Extra income can be allocated towards savings to accelerate your progress.

5. Should I prioritize paying off debt or saving?

Both paying off debt and saving are important financial goals. It’s generally recommended to prioritize high-interest debt repayment, such as credit card debt, as the interest charges can accumulate quickly. Once you have a plan in place to tackle your debt, you can simultaneously save for emergencies and other financial goals.

However, it’s crucial to strike a balance between debt repayment and saving. Allocating a portion of your monthly income towards savings ensures that you have a safety net for unexpected expenses and are working towards future financial goals. Consulting with a financial advisor can also provide guidance on the best approach based on your specific situation.

How Much Money You Need To Save By EVERY AGE

Final Summary: How Much Money Should You Save Each Month?

So, we’ve reached the end of our journey on the quest to determine how much money you should save each month. After diving into the world of personal finance and exploring various perspectives, it’s clear that there is no one-size-fits-all answer. However, there are some key principles that can guide us in making this decision.

First and foremost, it’s essential to prioritize your financial goals and align your savings accordingly. Whether you’re saving for emergencies, retirement, or a specific milestone like buying a house or starting a business, setting clear objectives will help you determine the right amount to save each month. Remember, it’s not just about the present but also about securing a stable and prosperous future.

Additionally, it’s crucial to strike a balance between saving and enjoying the present. While saving is important, it’s equally important to live your life and indulge in the things that bring you joy. By budgeting wisely, cutting unnecessary expenses, and finding ways to increase your income, you can find that sweet spot where you save enough while still savoring the present moment.

In conclusion, the amount of money you should save each month depends on your individual circumstances, goals, and priorities. Take the time to reflect on your financial situation and aspirations, and then create a savings plan that works for you. Remember, it’s not just about the destination, but also about the journey towards financial freedom and security