Retirement is a topic that often evokes mixed emotions. On one hand, it represents freedom, relaxation, and a chance to pursue long-awaited dreams. On the other hand, it can also bring uncertainty, financial concerns, and the need for careful planning. So, what is a simple retirement plan? In this article, we will delve into the world of retirement planning and explore the concept of a simple retirement plan that can help individuals navigate their way to a secure and fulfilling future.

When it comes to retirement planning, simplicity is key. A simple retirement plan is one that is easy to understand, implement, and maintain. It provides individuals with a clear roadmap for saving, investing, and managing their finances to ensure a comfortable retirement. Whether you’re just starting your career or nearing the end of it, having a simple retirement plan in place can give you peace of mind and a sense of control over your financial future. So, let’s dive in and discover the essentials of a simple retirement plan that can set you on the path to a worry-free retirement.

A Simple Retirement Plan, also known as a Savings Incentive Match Plan for Employees (SIMPLE) IRA, is a retirement savings plan designed for small businesses and self-employed individuals. It allows employees to make salary deferral contributions, which are tax-deductible, and employers can choose to match a percentage of those contributions. This plan offers a simplified administration process and lower costs compared to other retirement plans. It is a great option for those looking for an easy and accessible way to save for retirement.

What is a Simple Retirement Plan?

A simple retirement plan, also known as a Simplified Employee Pension (SEP) plan, is a retirement savings option for self-employed individuals and small business owners. It is designed to provide an easy and cost-effective way to save for retirement, offering tax advantages and flexibility.

How Does a Simple Retirement Plan Work?

A simple retirement plan allows employers to contribute to their own retirement accounts and their employees’ retirement accounts. Contributions are made on a pre-tax basis, reducing the employer’s and employees’ taxable income. The contributions are invested in a retirement account, such as an individual retirement account (IRA) or a 401(k) plan.

The employer has the flexibility to choose the contribution amount each year. Contributions can vary from year to year, depending on the financial situation of the business. However, there are contribution limits set by the Internal Revenue Service (IRS) to ensure fairness and prevent excessive contributions.

Benefits of a Simple Retirement Plan

A simple retirement plan offers several benefits for both employers and employees. Firstly, it provides a tax benefit by allowing contributions to be made on a pre-tax basis. This reduces the taxable income for both the employer and employees, resulting in lower tax liabilities.

Secondly, a simple retirement plan allows for flexible contributions. Unlike traditional pension plans, which require fixed contributions, a simple retirement plan allows employers to adjust the contribution amount each year based on the business’s financial performance. This flexibility is particularly beneficial for small businesses with fluctuating income.

Furthermore, a simple retirement plan helps attract and retain talented employees. Offering a retirement savings option demonstrates the employer’s commitment to their employees’ financial well-being and future. This can enhance job satisfaction and loyalty among employees.

How to Set Up a Simple Retirement Plan

Setting up a simple retirement plan is relatively straightforward. The first step is to establish the plan with the IRS by completing Form 5305-SEP or using an approved prototype plan document. The plan must be established by the employer’s tax filing deadline, including extensions.

Once the plan is established, the employer can start making contributions. Contributions can be made up until the employer’s tax filing deadline, including extensions. The employer must contribute the same percentage of compensation for all eligible employees, including themselves. However, the maximum contribution limit per employee may vary each year, as determined by the IRS.

It is essential to communicate the simple retirement plan to employees and provide them with the necessary information to participate. This includes explaining the contribution percentage, investment options, and vesting schedules, if applicable. Regular communication and education about the plan can help employees make informed decisions about their retirement savings.

Key Features of a Simple Retirement Plan

A simple retirement plan has several key features that make it an attractive option for self-employed individuals and small business owners. These features include:

1. Easy administration: Unlike traditional pension plans, which can be complex and costly to administer, a simple retirement plan has minimal administrative requirements. There are no annual filing requirements with the IRS, and the employer can handle the plan’s administration internally or through a financial institution.

2. Tax advantages: Contributions to a simple retirement plan are tax-deductible for the employer and tax-deferred for the employees. This means that contributions reduce the employer’s taxable income and employees’ taxable income. Taxes on the contributions and investment earnings are deferred until withdrawal during retirement.

3. Flexibility: A simple retirement plan offers flexibility in terms of contribution amounts. The employer can choose to contribute a fixed percentage of compensation each year or adjust the contribution based on the business’s financial situation. This flexibility ensures that contributions align with the business’s cash flow.

4. Minimal cost: Compared to other retirement savings options, such as a 401(k) plan, a simple retirement plan has lower administrative costs. There are no annual filing fees or extensive reporting requirements. This makes it an affordable choice for small businesses with limited resources.

5. Eligibility: Both employers and employees can participate in a simple retirement plan. Employers must contribute the same percentage of compensation for all eligible employees, including themselves. Eligible employees are those who are at least 21 years old, have worked for the employer in at least three of the past five years, and have earned a minimum amount of compensation as determined by the IRS.

Conclusion

A simple retirement plan is a valuable option for self-employed individuals and small business owners who want to save for retirement while enjoying tax advantages and flexibility. By understanding how a simple retirement plan works, its benefits, and how to set it up, employers can make informed decisions to secure their financial future and provide a valuable benefit to their employees. With its easy administration, tax advantages, and flexibility, a simple retirement plan is worth considering for those looking to build a nest egg for their retirement years.

Key Takeaways: What is a Simple Retirement Plan?

- A simple retirement plan is a financial strategy to save money for the future.

- It helps individuals set aside funds to support themselves after they stop working.

- Contributions to a simple retirement plan are often made through automatic deductions from an employee’s salary.

- These plans typically offer tax advantages, such as tax-deferred growth or tax-free withdrawals.

- Simple retirement plans can include options like individual retirement accounts (IRAs) or employer-sponsored 401(k) plans.

Frequently Asked Questions

Question 1: How does a Simple Retirement Plan work?

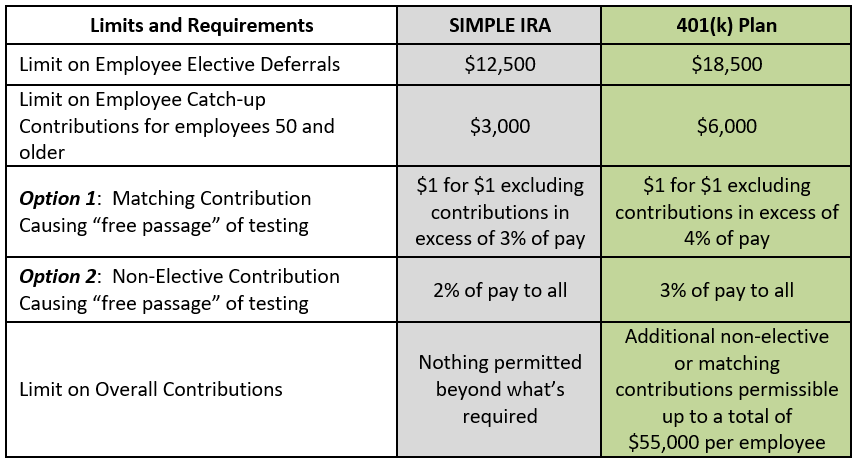

A Simple Retirement Plan, also known as a Savings Incentive Match Plan for Employees (SIMPLE), is a retirement plan designed for small businesses with fewer than 100 employees. It allows employees to make contributions to their retirement accounts through salary deferrals, and employers are required to make either matching contributions or non-elective contributions.

Under a SIMPLE plan, employees can contribute a percentage of their salary, up to a certain limit set by the IRS each year. Employers have the option to match the employee contributions dollar for dollar, up to a certain percentage of the employee’s salary, or contribute a fixed percentage of each employee’s salary, regardless of whether the employee contributes.

Question 2: What are the advantages of a Simple Retirement Plan?

One of the main advantages of a Simple Retirement Plan is its simplicity and ease of administration. It has fewer administrative requirements and costs compared to other retirement plans, making it an attractive option for small businesses.

Another advantage is the opportunity for employees to save for retirement through salary deferrals. The contributions made by employees are tax-deferred, meaning they are not subject to income tax until they are withdrawn during retirement. Additionally, employers have the option to make matching or non-elective contributions, which can help attract and retain talented employees.

Question 3: Are there any eligibility requirements for a Simple Retirement Plan?

Yes, there are eligibility requirements for both employers and employees to participate in a Simple Retirement Plan. Employers must have 100 or fewer employees who received at least $5,000 in compensation during the previous calendar year. They must also not maintain any other retirement plans.

Employees, on the other hand, must have received at least $5,000 in compensation during any two preceding calendar years and be expected to receive at least $5,000 in compensation during the current calendar year. They must also be employed by the employer maintaining the Simple Retirement Plan at any time during the calendar year.

Question 4: Can employees contribute to a Simple Retirement Plan and another retirement plan simultaneously?

Yes, employees can contribute to a Simple Retirement Plan and another retirement plan simultaneously. However, the total amount an employee can contribute to all retirement plans in a calendar year is subject to IRS limits. These limits are set to ensure that individuals do not exceed the maximum tax-deferred contribution allowed each year.

It’s important for employees to be aware of these limits and coordinate their contributions accordingly to maximize their retirement savings while staying within the allowable limits set by the IRS.

Question 5: Can a Simple Retirement Plan be converted to another retirement plan?

Yes, a Simple Retirement Plan can be converted to another retirement plan, such as a 401(k) plan. However, there are certain rules and requirements that need to be followed for this conversion to take place.

Employers should consult with a qualified retirement plan professional or financial advisor to understand the implications and procedures involved in converting a Simple Retirement Plan to another plan. It’s important to ensure that all legal and regulatory requirements are met during the conversion process.

Final Summary: What You Need to Know About a Simple Retirement Plan

Now that you have a better understanding of what a simple retirement plan entails, you can start taking the necessary steps to secure your financial future. Whether you’re just starting your career or nearing retirement age, having a retirement plan in place is crucial. Not only does it provide peace of mind, but it also allows you to enjoy your golden years without financial stress.

Remember, a simple retirement plan is designed to be accessible and easy to manage. It offers a range of benefits, including tax advantages and employer contributions. By contributing consistently and making informed investment choices, you can maximize the growth potential of your retirement savings.

So, take charge of your financial future today and start exploring the options available to you. Whether it’s an individual retirement account (IRA), a 401(k) plan, or a simplified employee pension (SEP) plan, there’s a retirement plan out there that suits your needs. Don’t wait until it’s too late – start planning for retirement now and enjoy the rewards later in life.