Have you ever wondered how to manage your finances effectively and save money without feeling overwhelmed? Well, let me introduce you to the 50 30 20 Budget Rule. This rule has gained popularity as a simple and practical method for budgeting your income. But what exactly does it entail? Let’s dive in and explore how this budgeting strategy can help you take control of your finances and achieve your financial goals.

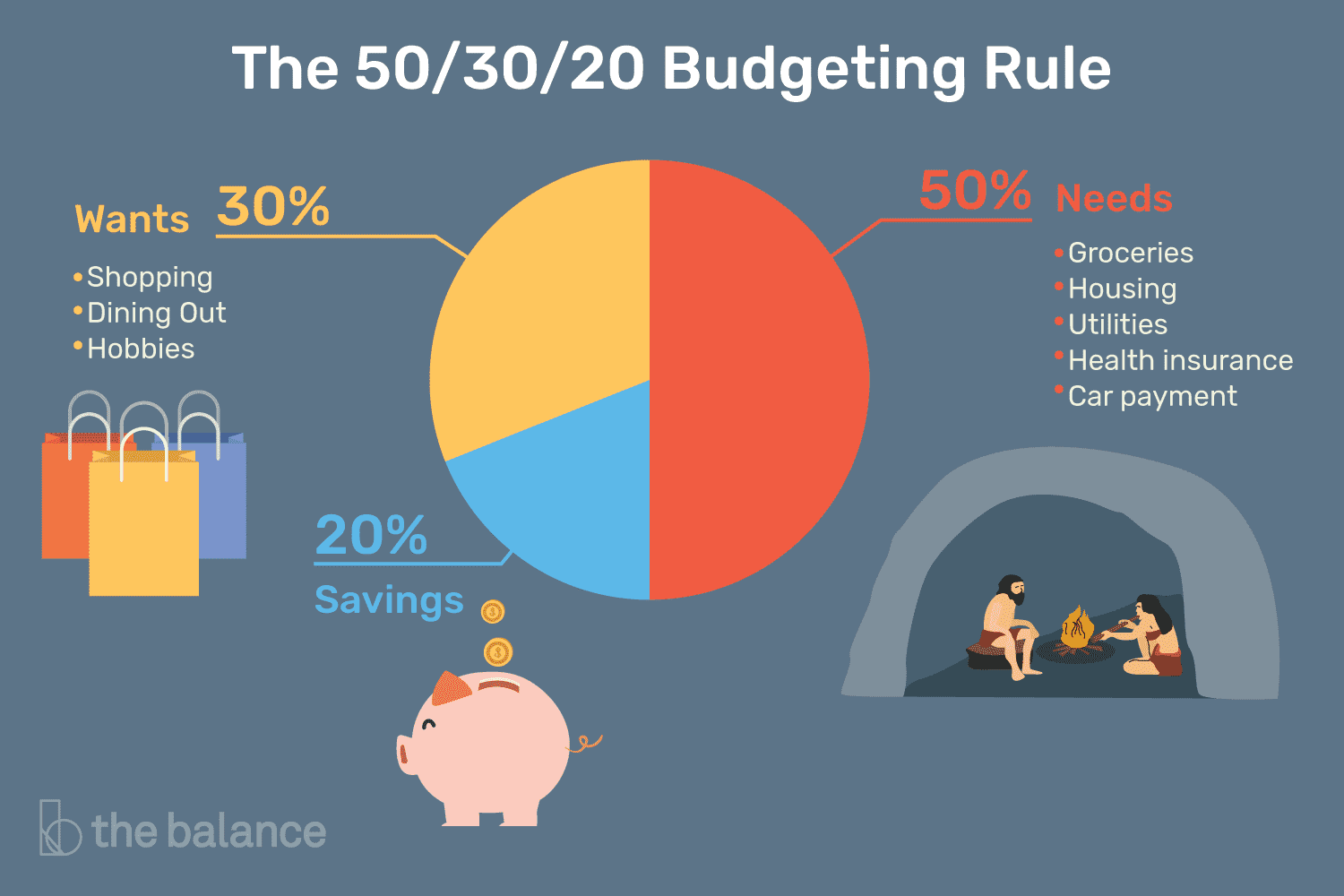

The 50 30 20 Budget Rule is a guideline that suggests dividing your after-tax income into three categories: needs, wants, and savings. The rule suggests allocating 50% of your income towards essential expenses such as housing, utilities, groceries, and transportation. These are the necessities that you need to live comfortably and maintain a stable lifestyle. The next 30% can be allocated towards discretionary spending, which includes things like dining out, entertainment, and non-essential purchases. This category allows you to enjoy life while still being mindful of your spending. Finally, the remaining 20% is dedicated to savings and debt repayment. This portion should be used to build an emergency fund, save for future goals, and pay off any outstanding debts. By following this budgeting rule, you can strike a balance between meeting your needs, enjoying your wants, and securing your financial future. So, let’s explore the 50 30 20 Budget Rule further and see how it can benefit you.

What is the 50 30 20 Budget Rule?

The 50 30 20 budget rule is a popular method of budgeting that helps individuals and households allocate their income effectively. This rule suggests that you divide your after-tax income into three categories: needs, wants, and savings. Specifically, 50% of your income should be allocated for needs such as housing, utilities, groceries, and transportation. The next 30% can be allocated for wants, such as dining out, entertainment, and non-essential purchases. Finally, 20% should be allocated for savings, including debt repayment, emergency funds, and retirement contributions.

This budgeting method is designed to provide a balanced approach to managing your finances. By prioritizing your needs and wants while also saving for the future, you can achieve financial stability and avoid overspending. The 50 30 20 budget rule can be customized to fit your specific circumstances, allowing you to make adjustments based on your income, expenses, and financial goals.

The Benefits of the 50 30 20 Budget Rule

Implementing the 50 30 20 budget rule offers several benefits for individuals and households. Firstly, it provides a clear and simple framework for budgeting. By dividing your income into three categories, you can easily track and manage your expenses. This budgeting method also promotes financial discipline by encouraging you to prioritize your needs and wants, which can help you avoid unnecessary debt.

Another benefit is that the 50 30 20 budget rule allows you to save for the future. By allocating 20% of your income to savings, you can build an emergency fund, pay off debt, and contribute to retirement savings. This helps you establish financial security and prepare for unexpected expenses.

How to Implement the 50 30 20 Budget Rule

Implementing the 50 30 20 budget rule is relatively straightforward. Start by calculating your after-tax income, which is the amount of money you take home after taxes and deductions. Once you have this figure, divide it into three categories: needs, wants, and savings.

For the needs category, allocate 50% of your income to cover essential expenses such as housing, utilities, groceries, and transportation. This ensures that you have enough to cover your basic needs each month. The wants category should receive 30% of your income, which can be used for discretionary spending like dining out, entertainment, and non-essential purchases. Finally, allocate 20% of your income to savings, which can include building an emergency fund, paying off debt, and contributing to retirement accounts.

The Importance of Tracking and Adjusting

While the 50 30 20 budget rule provides a helpful framework, it’s important to regularly track your expenses and make adjustments as needed. Keep a record of your spending to ensure that you’re staying within the allocated percentages for needs, wants, and savings. If you find that you’re consistently overspending in one category, you may need to make adjustments to bring your budget back into balance.

Additionally, as your income or expenses change, you may need to adjust the percentages allocated to each category. For example, if you receive a raise or start earning additional income, you may choose to allocate a higher percentage to savings. Similarly, if your expenses increase, you may need to adjust the percentages to ensure that you’re still able to cover your needs while maintaining your savings goals.

Key Takeaways: What is the 50 30 20 Budget Rule?

- The 50 30 20 budget rule is a simple method for managing your finances.

- It suggests dividing your income into three categories: needs, wants, and savings.

- 50% of your income should be allocated for essential needs like rent, bills, and groceries.

- 30% should be set aside for discretionary wants like dining out or entertainment.

- 20% should be saved for future goals, such as emergencies or retirement.

Frequently Asked Questions

The 50 30 20 budget rule is a popular budgeting method that helps individuals allocate their income towards different categories to achieve financial stability. It suggests that 50% of your income should be allocated towards essential expenses, 30% towards discretionary spending, and 20% towards savings and debt repayment. Here are some common questions about the 50 30 20 budget rule:

Question 1: How do I determine my essential expenses?

Essential expenses include your basic needs such as housing, utilities, transportation, groceries, and healthcare. To determine your essential expenses, start by listing all your fixed monthly bills. This includes rent or mortgage payments, utility bills, insurance premiums, and any other necessary expenses. Once you have a clear idea of your fixed expenses, estimate your variable expenses such as groceries and transportation costs. Add up these expenses to get your total essential expenses.

Remember, the goal is to keep your essential expenses within 50% of your income. If your essential expenses exceed this threshold, you may need to reassess your budget and consider ways to reduce your spending in this category.

Question 2: What does discretionary spending include?

Discretionary spending refers to non-essential expenses that are not necessary for your basic needs. This category includes expenses such as dining out, entertainment, travel, shopping, and hobbies. It’s important to allocate 30% of your income towards discretionary spending to maintain a balance between enjoying your money and saving for the future.

When determining your discretionary spending, consider your lifestyle and priorities. If you enjoy dining out frequently or traveling often, allocate a larger portion of your budget towards discretionary spending. However, if you prefer to save more or have financial goals, you may choose to allocate a smaller percentage towards discretionary spending.

Question 3: How should I allocate the remaining 20% of my income?

The remaining 20% of your income should be allocated towards savings and debt repayment. This category includes building an emergency fund, saving for retirement, paying off debt, and investing for the future. It’s important to prioritize saving and debt repayment to achieve long-term financial stability.

When allocating this 20%, consider your financial goals and prioritize them accordingly. Start by building an emergency fund that covers at least three to six months of living expenses. Once you have established your emergency fund, focus on paying off high-interest debt, such as credit card debt. Finally, consider investing for retirement or other long-term goals to grow your wealth over time.

Question 4: Can I customize the percentages of the 50 30 20 budget rule?

Yes, the percentages of the 50 30 20 budget rule can be customized based on your individual circumstances and financial goals. While the rule suggests a balanced allocation of 50% for essential expenses, 30% for discretionary spending, and 20% for savings and debt repayment, you can adjust these percentages to fit your needs.

For example, if you have high rent or mortgage payments, you may need to allocate a larger percentage towards essential expenses. Similarly, if you have specific financial goals such as saving for a down payment on a house or paying off student loans, you can allocate a larger percentage towards savings and debt repayment. The key is to find a balance that works for you and helps you achieve your financial objectives.

Question 5: How do I track and manage my budget using the 50 30 20 rule?

Tracking and managing your budget using the 50 30 20 rule can be done through various methods. Start by creating a detailed budget that outlines your income, expenses, and savings goals. You can use budgeting apps or spreadsheets to track your expenses and ensure you are staying within the allocated percentages.

Regularly review your budget and make adjustments as needed. If you find that you are consistently overspending in a particular category, you may need to reassess your spending habits and find ways to cut back. Additionally, it’s important to regularly monitor your savings goals and debt repayment progress to stay on track towards financial stability.

50/30/20 Budgeting Rule and How to Use It

Final Thoughts on the 50/30/20 Budget Rule

Now that we’ve explored the ins and outs of the 50/30/20 budget rule, it’s clear that this approach can be a game-changer when it comes to managing your finances. By allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment, you can strike a balance between enjoying your present and securing your future.

The beauty of the 50/30/20 budget rule lies in its simplicity and flexibility. It provides a clear framework for budgeting without being overly restrictive, allowing you to make conscious choices about your spending while still leaving room for enjoyment. It encourages you to prioritize your needs, indulge in your wants within reason, and establish a solid financial foundation.

By following this budgeting rule, you can avoid the stress and anxiety that often accompany financial uncertainty. It empowers you to take control of your money, set realistic goals, and make informed decisions about your spending habits. Remember, it’s never too late to start budgeting and working towards a more financially secure future. So why not give the 50/30/20 budget rule a try and see how it can transform your financial well-being? Your future self will thank you!